Microsoft – Are the Windows Closing?

Why I'm less bullish on one of the highest quality franchises.

Microsoft has undoubtedly been one of the most exceptional companies in modern history. Windows is the default operating system for personal computing, Office is the core productivity layer for organisations globally, and Azure serves as the critical cloud infrastructure that powers software and AI today. The company has played a central role in the development and proliferation of modern technology and its impact to the world cannot be understated.

Over the years, Microsoft has repeatedly deployed a successful playbook of building platforms to become more relevant to more people. This success has been rightly reflected in the company’s over $3tn market capitalisation today and spectacular long-term returns.

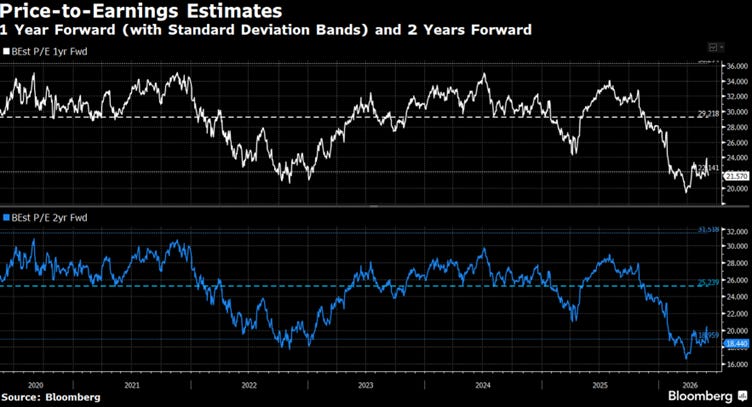

Today, the business trades at a 21.5x forward P/E multiple, only slightly above the S&P500’s multiple of 20.5x. Yet it is expected to grow earnings at a rate of 18% p.a. over the next two years and is far higher quality relative to the average S&P500 business. Seems like a no-brainer right?

My view on the long-term trajectory of Microsoft’s moat has actually soured over the past few months. It might seem like heresy to say this especially when prominent investors such as Bill Ackman have taken significant long positions in the business. But I think the calculus around risk/reward is changing at the margins such that I am less bullish on the business than I once was. Below I outline three reasons for why I believe this to be the case.

From capital-light to capital-hungry

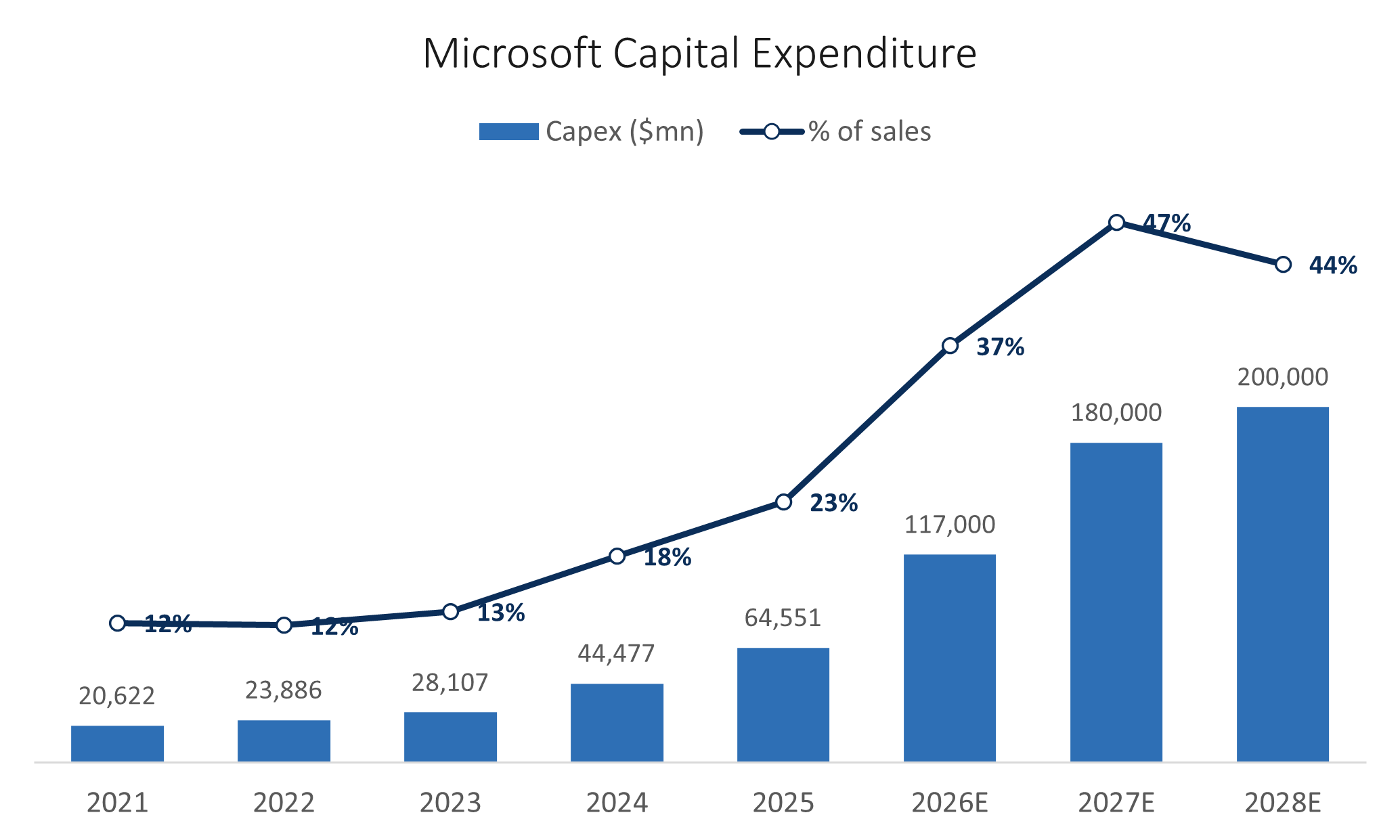

The graph above shows Microsoft’s annual capex over the past five fiscal years, alongside the projected spending over the next three (note we are already three quarters in FY26). Analysts expect the company to spend close to $500bn between FY26 and FY28. In FY27 alone, Microsoft could spend roughly as much as it did across FY21 to FY25 combined. This represents a staggering pace and quantum of investments for what has historically been a relatively capital light business.

Of course, the spend itself is not the central issue. What matters is the return Microsoft can generate on that investment. Thus far, there’s little evidence to suggest this is a poor use of capital. Azure continues to grow at a 40% rate and likely earns very healthy operating margins (despite some gross margin pressure from the infrastructure build-out). The useful life of these assets may also exceed their six-year depreciating schedule, while some of the infrastructure should remain fungible across customers and workloads.

However, several questions arise as we look out further into the future:

1. Is Microsoft overbuilding capacity?

2. Are investments being made near the top of the cycle?

3. How quickly will capex continue to grow and what impact does this have on FCF?

4. What return can investments in these assets sustain over a decade?

5. Can Microsoft continue to largely self-fund its capex or will it become more reliant on capital markets?

These questions are all open to debate and much has already been written on them. The broader point here is that they were largely absent from my original thesis for Microsoft. Outside Xbox and Windows, which both retain some exposure to hardware cycles, the business was neither particularly capital intensive nor especially cyclical. That appears to be changing rapidly.

The cyclicality may not yet be visible, but it would be imprudent to assume that demand for tokens will follow a smooth exponential curve indefinitely. AI demand may ultimately justify the investment, but the path is unlikely to be linear. Periods of constrained supply could be followed by excess capacity, falling compute costs or slower workload growth. The risk is not necessarily that demand disappears, but that supply is built ahead of demand and returns temporarily compress.

This does not mean Microsoft is misallocating capital. The company may be rationally investing ahead of a large and enduring opportunity. However, the range of possible outcomes has widened. Investors must now assess not only the growth of demand, but also utilisation rates, asset obsolescence, customer concentration and the durability of returns on each new dollar invested.

That is a materially different exercise from valuing a capital-light software company with recurring revenue and limited reinvestment needs. Microsoft may still deserve a premium valuation, but the composition of its earnings is changing. As more value is generated through infrastructure, the appropriate multiple should increasingly reflect the risks that come with owning infrastructure.

Renting GPUs vs. running the enterprise

This brings me to my second point: what is the right multiple to pay for a business that is more capital intensive and potentially more cyclical?

My mental shortcut for Microsoft has always been to equate the company with software. Perhaps that thinking is a bit antiquated, considering the decade-plus investment the business has made in scaling its Azure. Broadly, however, we can think about Microsoft providing enterprises with large, deeply embedded IT platforms. Windows is a platform for personal and enterprise computing, Office is a platform for productivity and collaboration, Azure is a platform for computing and data storage.

The important point is that these platforms are not interchangeable pieces of infrastructure. They sit inside the daily operating fabric of a business. Enterprises build workflows around them, train employees on them, integrate third-party tools into them and embed security, compliance and identity management around them. That makes Microsoft’s revenue base unusually durable because the customer is not merely buying compute or storage. It is buying continuity, familiarity, interoperability and reduced operational risk.

This is what has historically made Microsoft such a valuable business. A platform that becomes the system of work, benefits from high switching costs and deep customer dependency. The economic value is not just in the product itself, but in the ecosystem that forms around it. Windows, Office and Azure have each benefited from this dynamic in different ways. They are not commodities because customers are not making purchasing decisions purely on price.

The question is whether AI infrastructure revenue carries the same characteristics. With growing share of Azure’s revenue coming from LLM companies consuming enormous amounts of GPU capacity, the nature of the business may be subtly different. In that case, Microsoft is not necessarily providing a deeply embedded enterprise platform. It is providing scarce infrastructure to customers whose primary attachment is to compute availability, price, performance and scale. Those are valuable attributes, but they are less clearly unique.

This distinction matters because customers such as OpenAI, Anthropic or other AI labs are not necessarily locked into Azure in the same way a large enterprise is locked into Microsoft’s productivity, identity, security and cloud estate. In theory, model companies can move workloads across hyperscalers if the economics, capacity or technical performance are better elsewhere. That does not make the revenue unattractive, but it may make it less platform-like. It is closer to being a provider of critical infrastructure than a provider of an irreplaceable application layer.

That creates a tension in how the market should value Microsoft. The company may still be one of the biggest beneficiaries of AI, but the quality of that incremental revenue is arguably worse. Revenue generated from scarce infrastructure can be high growth, but it is also more capital intensive, potentially more competitive and more exposed to supply and demand cycles. Ultimately, this will be reflected in the multiple investors are willing to pay.

Betting the thesis on two labs

A key pillar of my original investment thesis was the breadth of earnings streams Microsoft enjoyed. That seems to be unravelling especially as a greater proportion of earnings are derived from the Azure business.

Now this isn’t necessarily a surprise given Azure has grown at an average rate of 40% p.a. over the past five years whilst the rest of the business has grown slower. Mathematically, it must constitute a larger proportion of the base over time. However, as I mention above, the quality of those revenues is quickly augmenting in a way that I would be more hesitant to apply the same multiple in prior years.

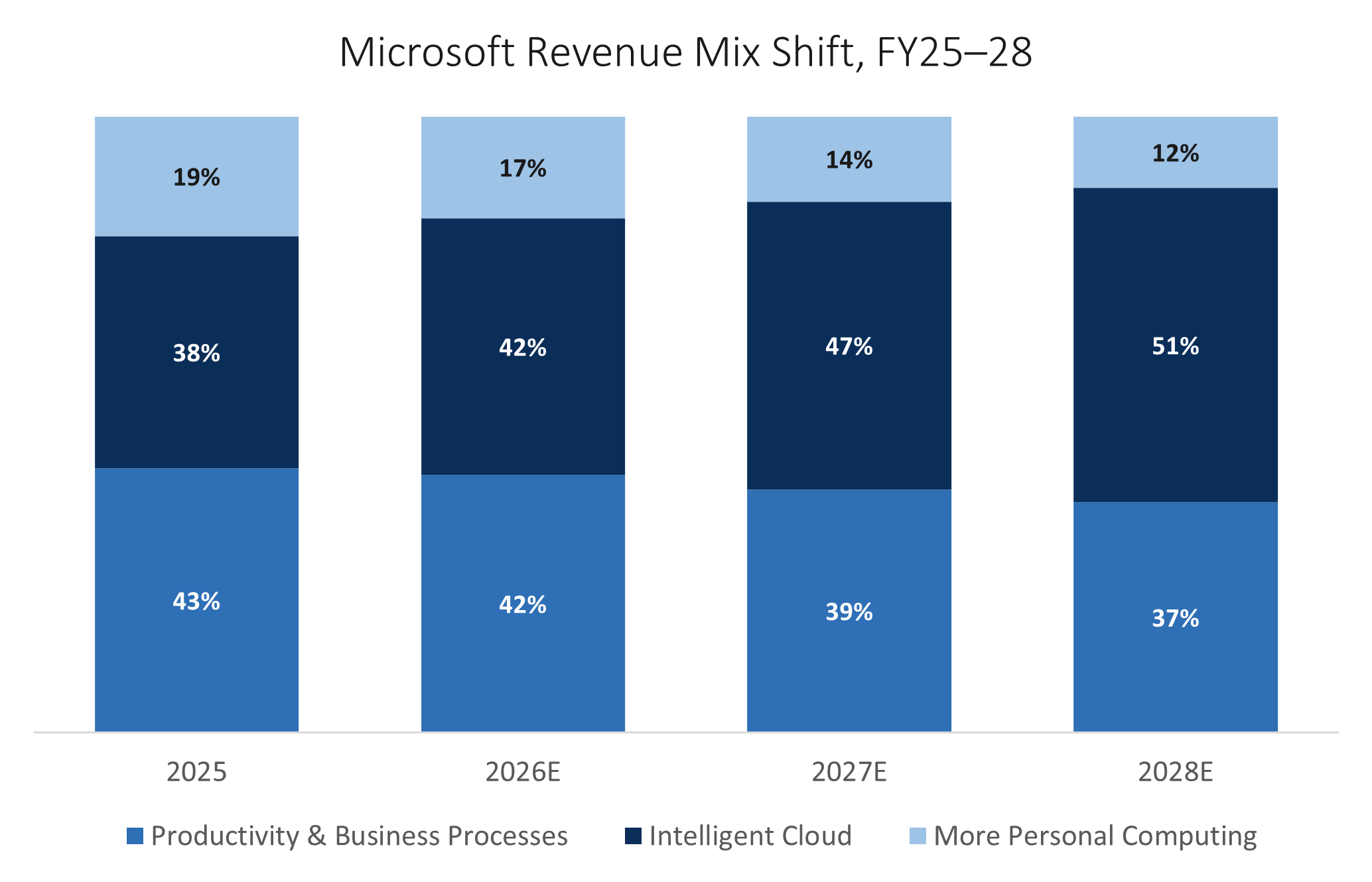

As of the end of FY25, revenues across Microsoft’s three reportable segments are fairly balanced with the majority of earnings stemming from core platforms such as Office, Dynamics and LinkedIn. However, if we project out to 2028 (I am using consensus estimates here), we can see that over 50% of revenues will be generated by the cloud segment alone.

Double clicking into the composition of growth within the cloud segment, we observe that a significant amount is being generated from AI workloads. In its most recent Q3 call, management called out that AI workflows have surpassed a $37bn ARR. Most sell-side analyst estimates peg that number to be in the mid-to-high $20bn range for FY26 and growing close to 100%. At this pace of growth, in FY28 that will be over $80bn or between 15-20% of total group revenues.

Again, this isn’t necessarily bad, but let’s consider the prior makeup of cloud revenues to the incremental dollar that is flowing through. Previously, Azure growth was driven by thousands of corporations shifting on-premise compute to Microsoft’s public cloud. They architected their business around Microsoft’s offerings and no single enterprise represented a meaningful share of those revenues. Compare that to the AI workloads which are primarily driven by the inference and training requirements of two companies – OpenAI and Anthropic.

Now even in FY28, it would be a far cry to suggest Microsoft is suffering from massive customer concentration. OpenAI and Anthropic would at most make up 5-10% of total group revenues each and these are high-margin, high growth streams of revenue. But let’s assume AI continues to follow its exponential curve and take a minute to do the mental exercise of considering Microsoft’s revenue mix in 2035 and beyond. That picture looks very different to what we see today.

Crucially, the relationship between frontier model developers and hyperscalers differs from Microsoft’s relationship with its core enterprise customers. These companies do not rely on Azure as their system of work, nor are they necessarily wedded to its broader software architecture. What they need above all is access to enormous amounts of compute, which in turn requires capital, power, chips, networking capacity and considerable expertise in building and operating large-scale data centres.

In this sense, Microsoft’s role is closer to that of an infrastructure sponsor than a traditional technology platform. It absorbs much of the upfront capital burden and provides scarce compute capacity at a scale few model developers could initially finance or operate themselves. That relationship is still valuable, but the source of dependency is different. The model developer relies on Microsoft because replicating the infrastructure is difficult and expensive, not because its organisation has been built around Azure.

Over time, however, that calculation may change. As model developers become larger, better funded and more confident in their future utilisation, the economics of owning or directly controlling infrastructure become more attractive. At sufficient scale, the margin paid to a hyperscaler may exceed the benefits of outsourcing. xAI’s development of Colossus illustrates the direction of travel.

This does not mean that model developers will become entirely independent. They will still depend on chipmakers, utilities, data-centre operators and external capital, while hyperscalers retain meaningful advantages in procurement and execution. The more credible risk is that the largest customers gradually diversify providers, build dedicated capacity and negotiate away some of the hyperscaler’s economics. Microsoft may therefore retain the workload without retaining the same degree of customer dependency or pricing power that characterises its traditional enterprise platforms.

As the Microsoft investment thesis becomes increasingly dependent on the returns generated from AI workloads, a new concentration risk is emerging. That greater uncertainty should command a higher risk premium, and all else equal, a lower multiple on future earnings.

Conclusion

I don’t mean to sound alarmist or suggest liquidating your shares in Microsoft (indeed I still have a position myself). I also certainly don’t mean to suggest Microsoft is a poor business or that its capital is being misallocated. It remains one of the highest-quality franchises in the world and a genuine beneficiary of the shift to AI.

The nuance here is that the character of the business is changing. A company once defined by capital-light, recurring software revenue and deeply embedded platforms is becoming more capital intensive, more cyclical and more reliant on a narrower set of infrastructure-led earnings whose customers are not necessarily locked in the way enterprises are.

Each of these shifts pulls in the same direction. Widening the range of outcomes and weakening the durability that justified Microsoft’s premium. The investment may still work, but it is no longer the same investment. As I see it, the windows are not closing, but they are narrowing.